Context

Towards the end of 2014 I was asked to become Customer Experience Lead for a large scale project around home ownership: Wonder.

This was meant to become a platform for investors, owner occupiers and those who are about to enter the house market.

At the time this was the biggest digital transformation project at Westpac.

It was treated as a Service Design project since it extended throughout the whole home ownership journey and across different channels.

The challenge

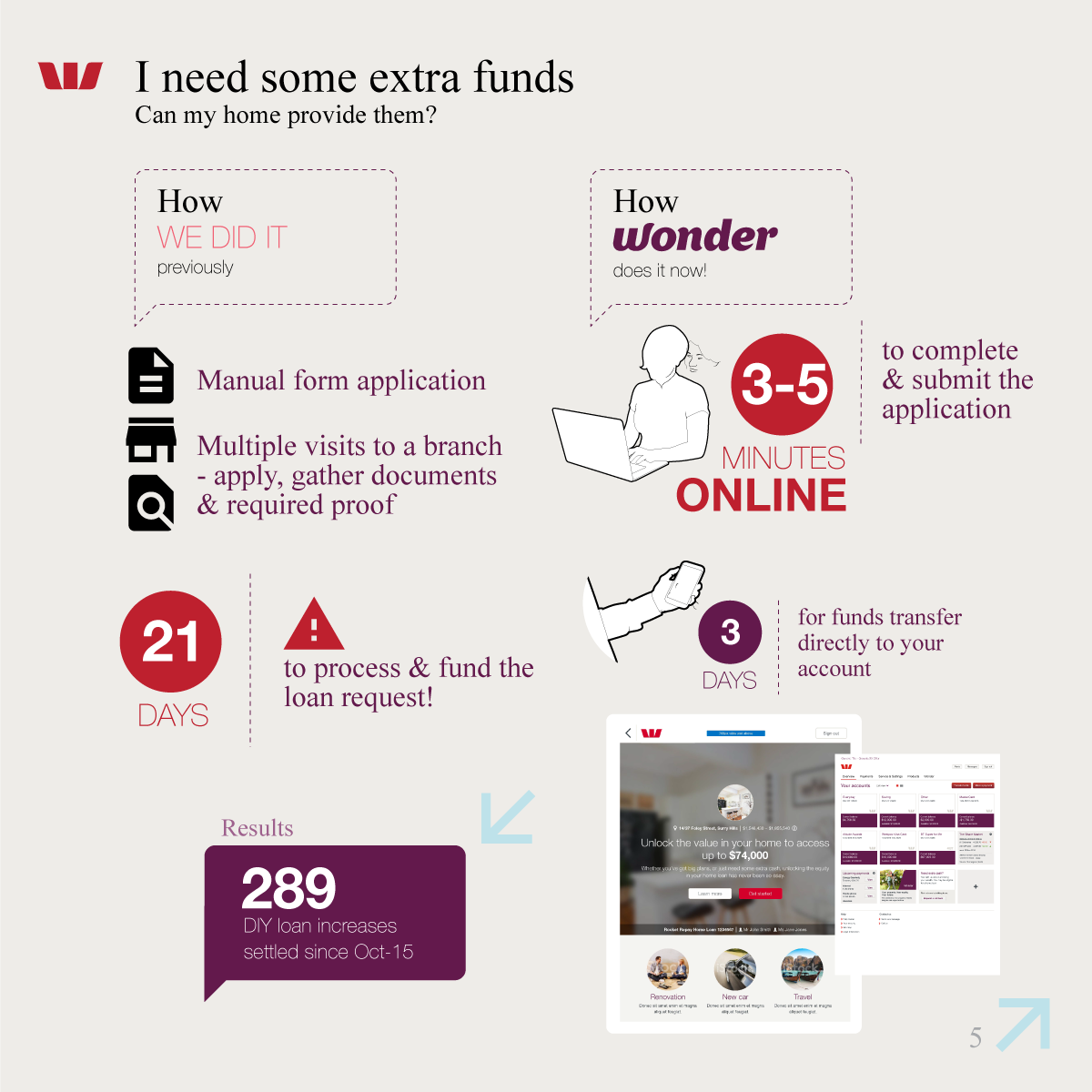

Before Wonder, the process for applying for a home loan was the same for all customers, whether they were new to the bank or long standing customers.

This is how that process looked:

- Fill out a paper form

- Submit this form to a banker in branch, coupled with supporting documentation such as proof of identity and assets

- Wait for a credit decision to be made, with fingers crossed that they received the outcome they wanted.

Whiteboarding & Personas

As a multi-disciplinary team we were looking to streamline this and solve some of Westpac's core business problems:

- How to could we use data to the advantage of the customer, taking data fragmentation, privacy and security limitations into consideration?

- How could we streamline the application process, what are current barriers and how could we take these away?

- What are the typical insights customers need to take key decisions around home ownership?

- When and where do we provide these insights? what can we base them upon?

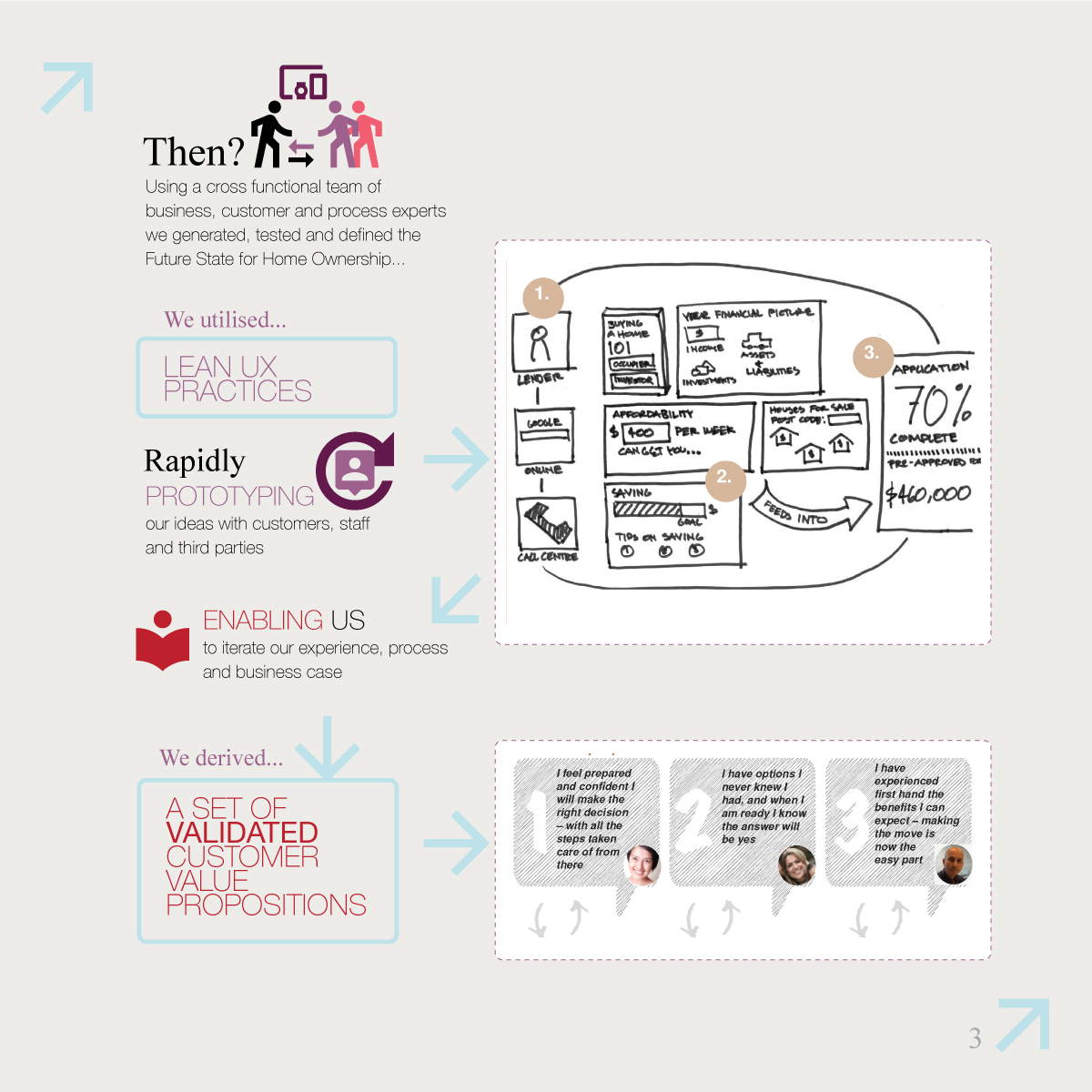

Approach

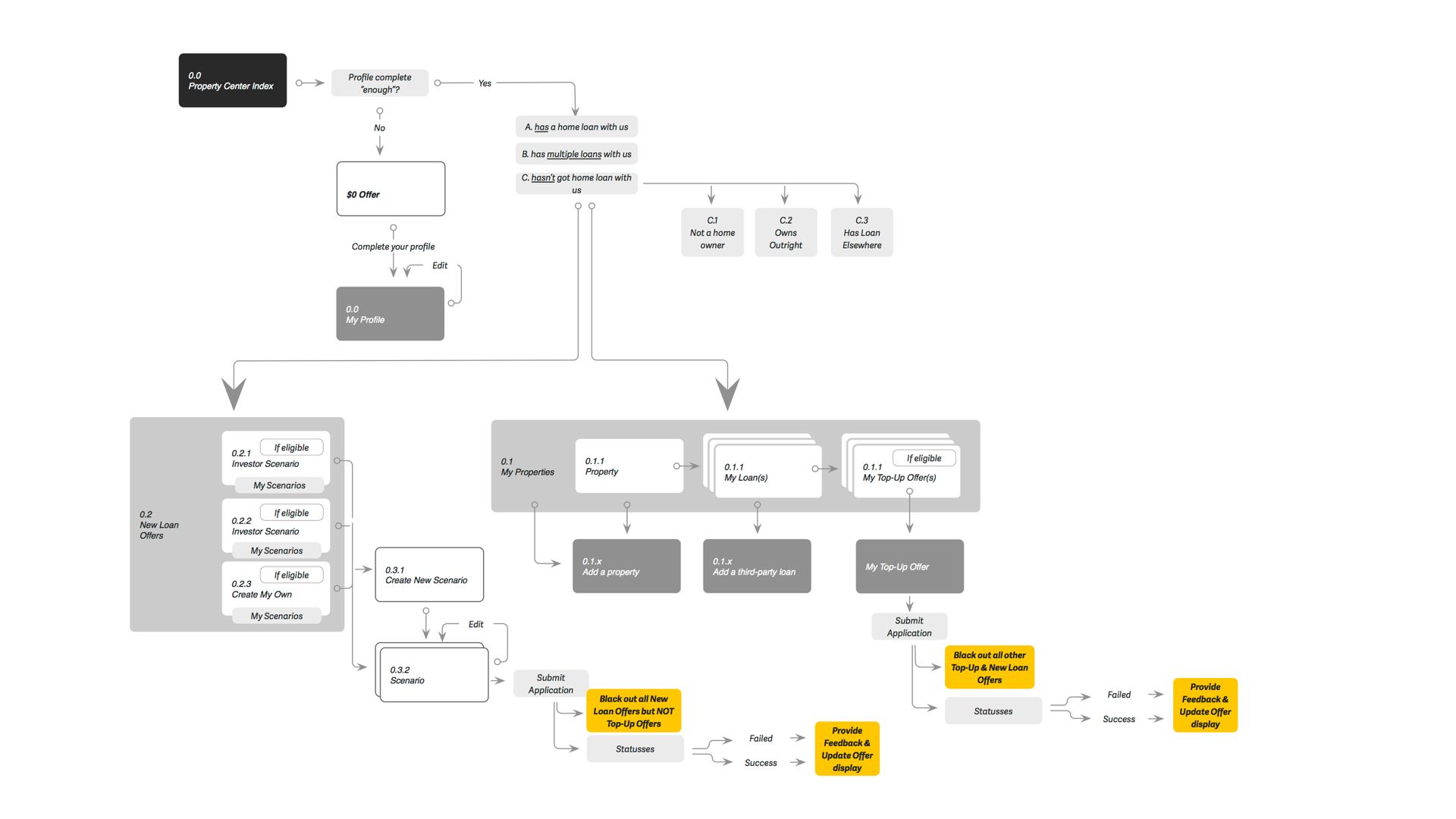

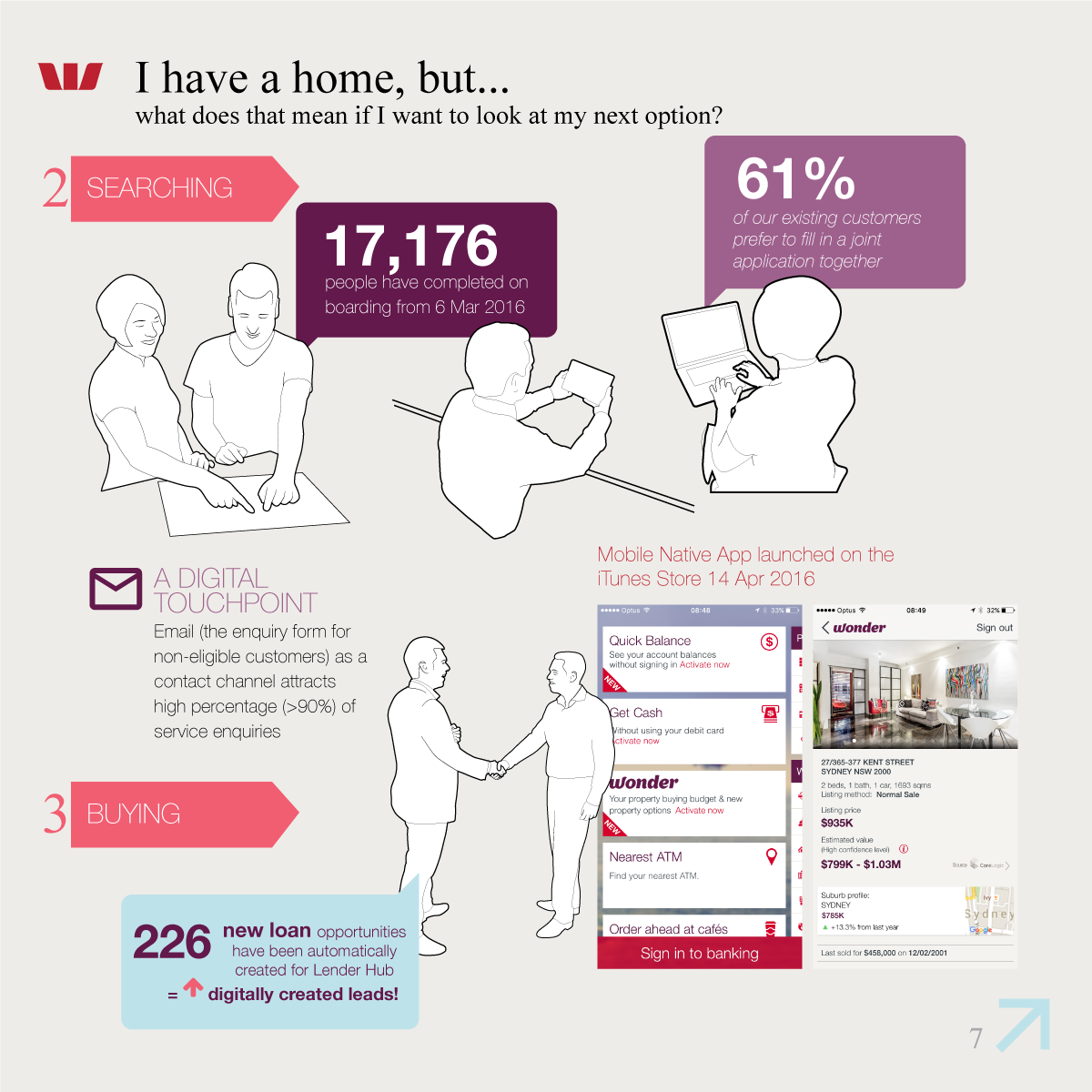

As a Customer Experience Lead I was responsible for giving shape to what was referred to as the “Property Center”, the "home" of Wonder.

We envisioned this as a functionality that would sit in, and closely integrate with, the pre-existing online banking suite of apps and websites.

Besides the stream of work I was responsible for, there were also two other big streams of work: one revolving around new loans and another one around increasing existing loans.

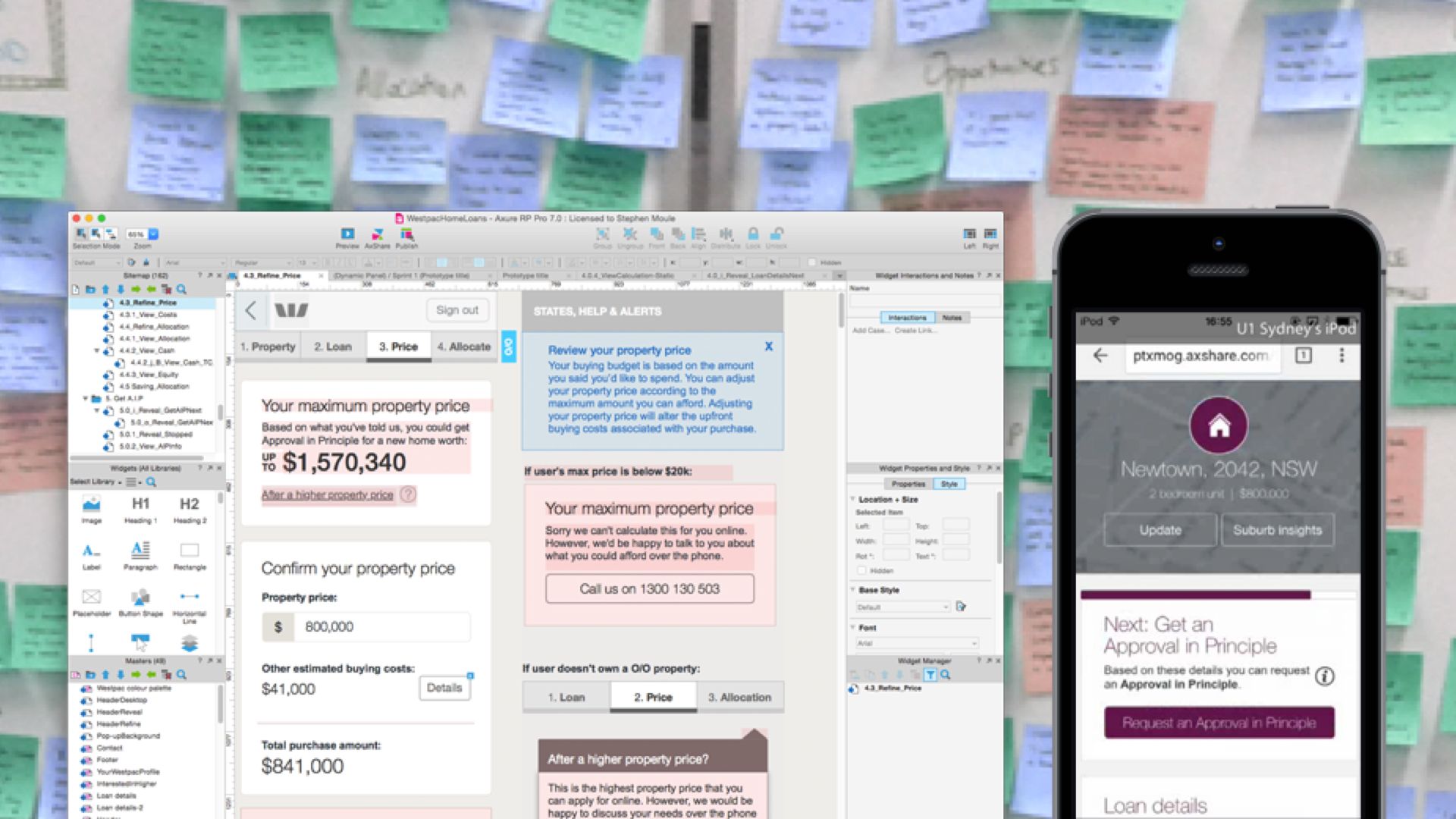

Sitemap & Axure Prototyping

Each stream had it's own UX, UI and development team and we all aligned with eachother on daily basis. Every team also committed to fortnightly user testing. The process we followed is roughly outlined below:

1. Observation, 2. Framing the Challenge, 3. Lean UX, 4. Customer Value Proposition, 5. Scenario A: Extra Funds, 6. Secario B: Next options 1/3, 7. Secario B: Next options 2/3, 8. Secario B: Next options 3/3

I led a team of UX and UI people and together we participated in bi-weekly Agile (SCRUM) sprints assisted by a team of developers. Our concepts were externally tested at the end of each sprint and it was my responsibility to process the findings and distill them into recommendations which I presented to the stakeholders.

The latest insights from our bi-weekly testing sessions were centrally displayed on a whiteboard.

Customer Research

To gather customer needs we organised interview sessions during which we:

- Asked a variety of questions around home ownership

- We talked them through various proposition variants and asked which they found most applealing and why

- Finally we did concept testing: mockups of different features and asked them about their thoughts

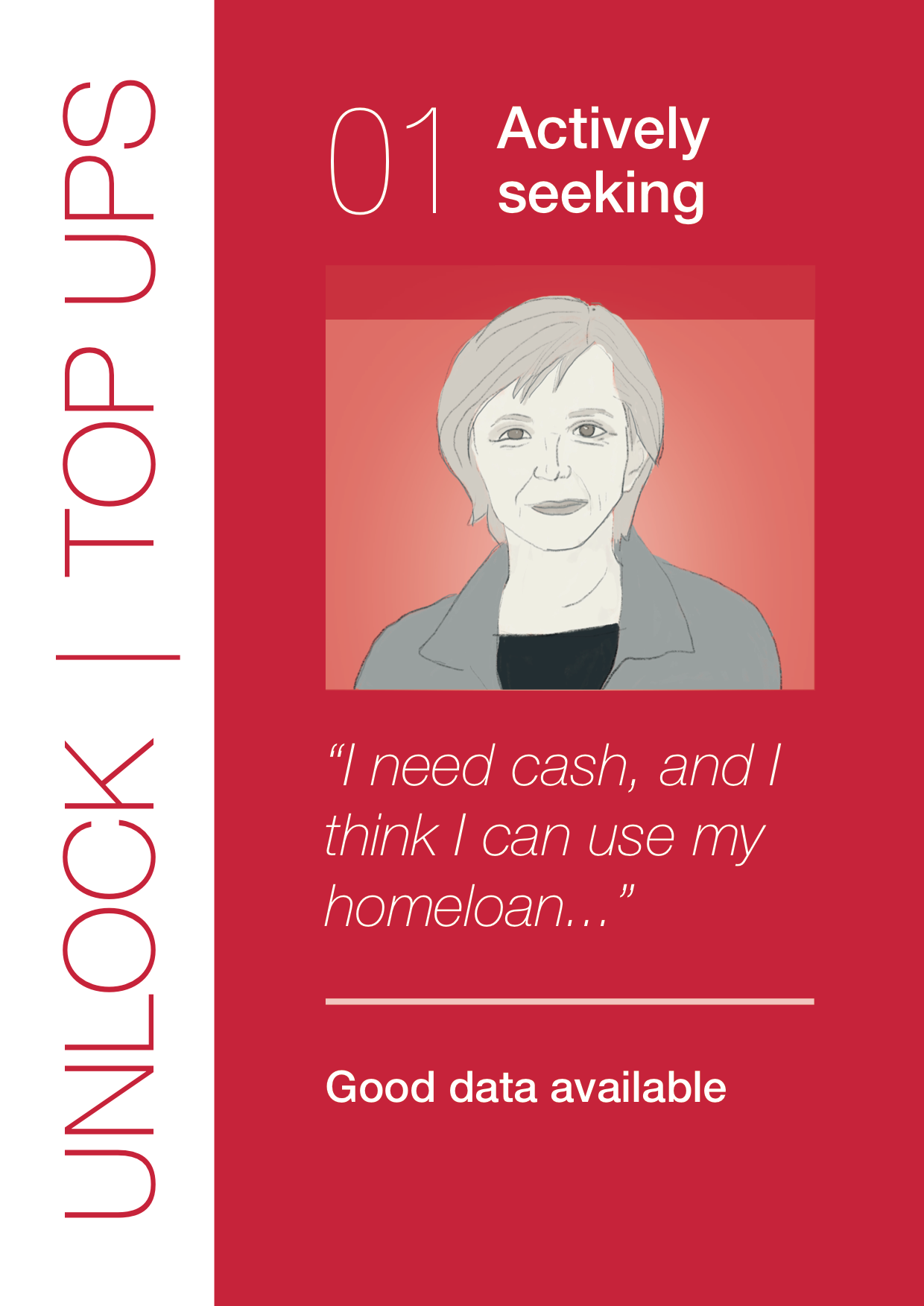

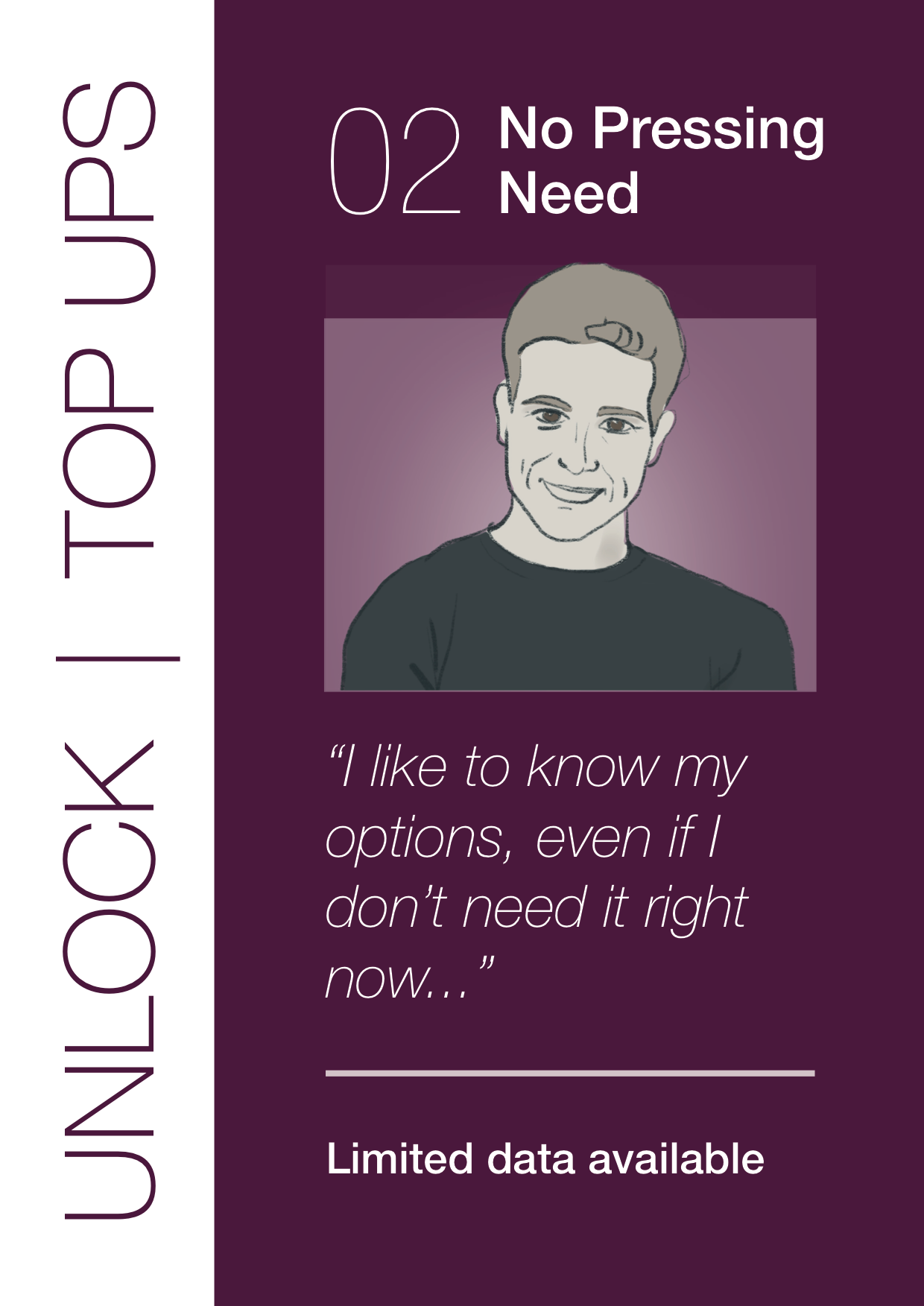

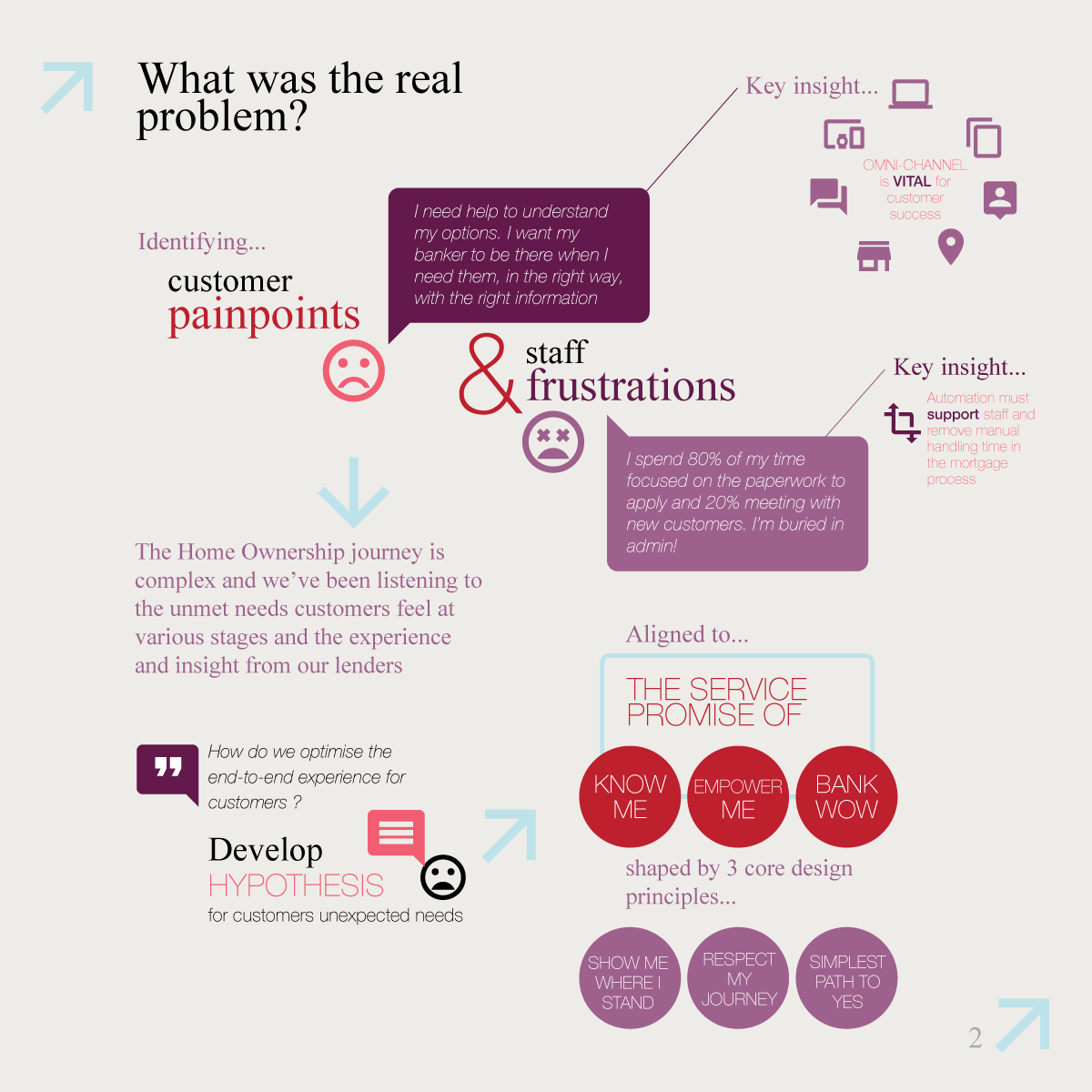

Key Customer Insights

We distilled our customer research into insights that fitted in 6 different categories of needs:

- I need an overview — A place where I can go to see all my nances from all my banks in one place: Cash on hand, the value of all my assets, liabilities and your net wealth.

- I need to understand — A place where I can go to understand where all my money is going and what I could change to improve my spending habits.

- I want to manage my goals — A place where I can go to set and track my savings goals.

- I want to optimise my finances — A place where I can go that helps me ensure my money is working as hard as it can for me.

- How much can I borrow? — A place where I can go to see how much money I can borrow for a home loan.

- I want to know what my options are — A place where I can go to see all the savings and investment options available to me

Customer principles

The entire Wonder experience was shaped by three core design principles. These were generated from the customer needs that we had distilled from our research and testing:

Show me where I stand; Customers want to understand the truth about their current borrowing capabilities.

Respect my journey; Customers want to access all the information important for them, before making such an important commitment.

Simplest path to yes; simplified data entry requirements and the inbuilt risk decision engine mean Wonder can offer customers a quick path to acting with confidence.

The housing market in 2015

It's important to mention that this project had a high importance within the organisation. Not just because home loans were big business, that's obvious. But also because the market was at a high point (see graph below). Affordability was still quite good but the actual house prices were going up in big steps. The housing market in Australia hasn't seen the crisis the rest of the world has. It's actually been on a steady incline since the 70s. There is an ongoing debate about whether the current market is a bubble. So in other words: the timing was right.

Solution

Overview

If we had learned one thing than it would be that owning a home is still the big dream for many Australians, but the many hurdles on the way made it often difficult for them.

The ambition for Wonder was to make things easier and act as a one-stop-shop.

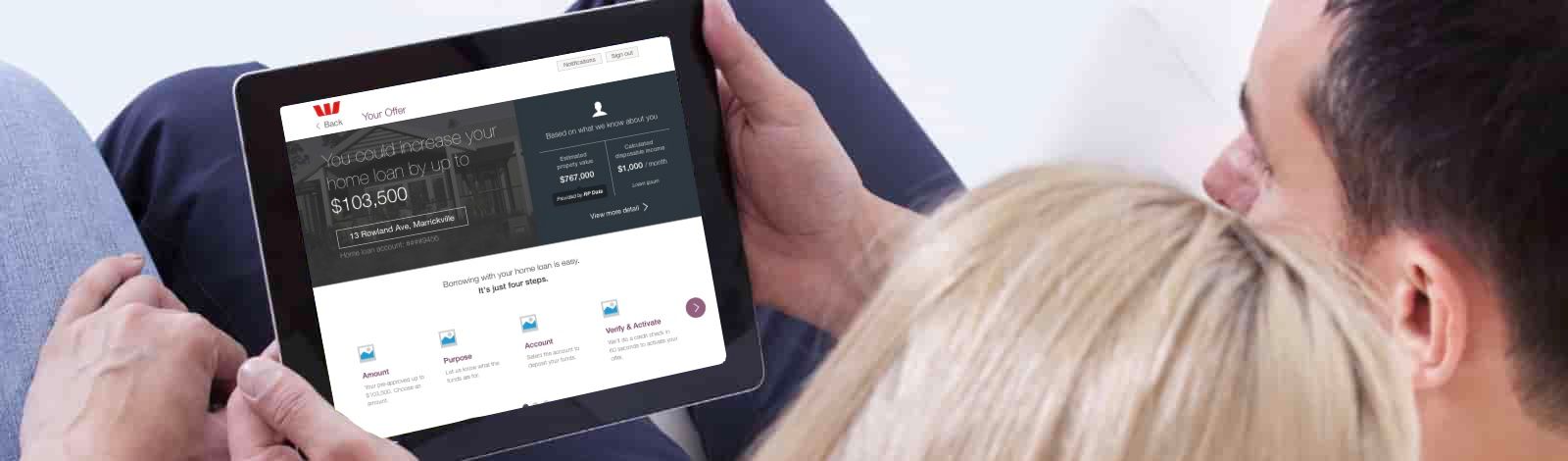

An up-to-date customer profile attached to a real time risk decision engine using regulator approved responsible lending practices gave customers a clear understanding of their borrowing options.

With each interaction with the bank, from a lending product to a credit card, Westpac collected important information about a customer’s position and used this to populate their profile. Based on that information, the risk engine calculated a live lending figure: this was the home loan the customer was able to lend.

As customers updated their profile with information such as a salary increases, or a credit card with another bank, that figure was updated in real time.

Scaling the product

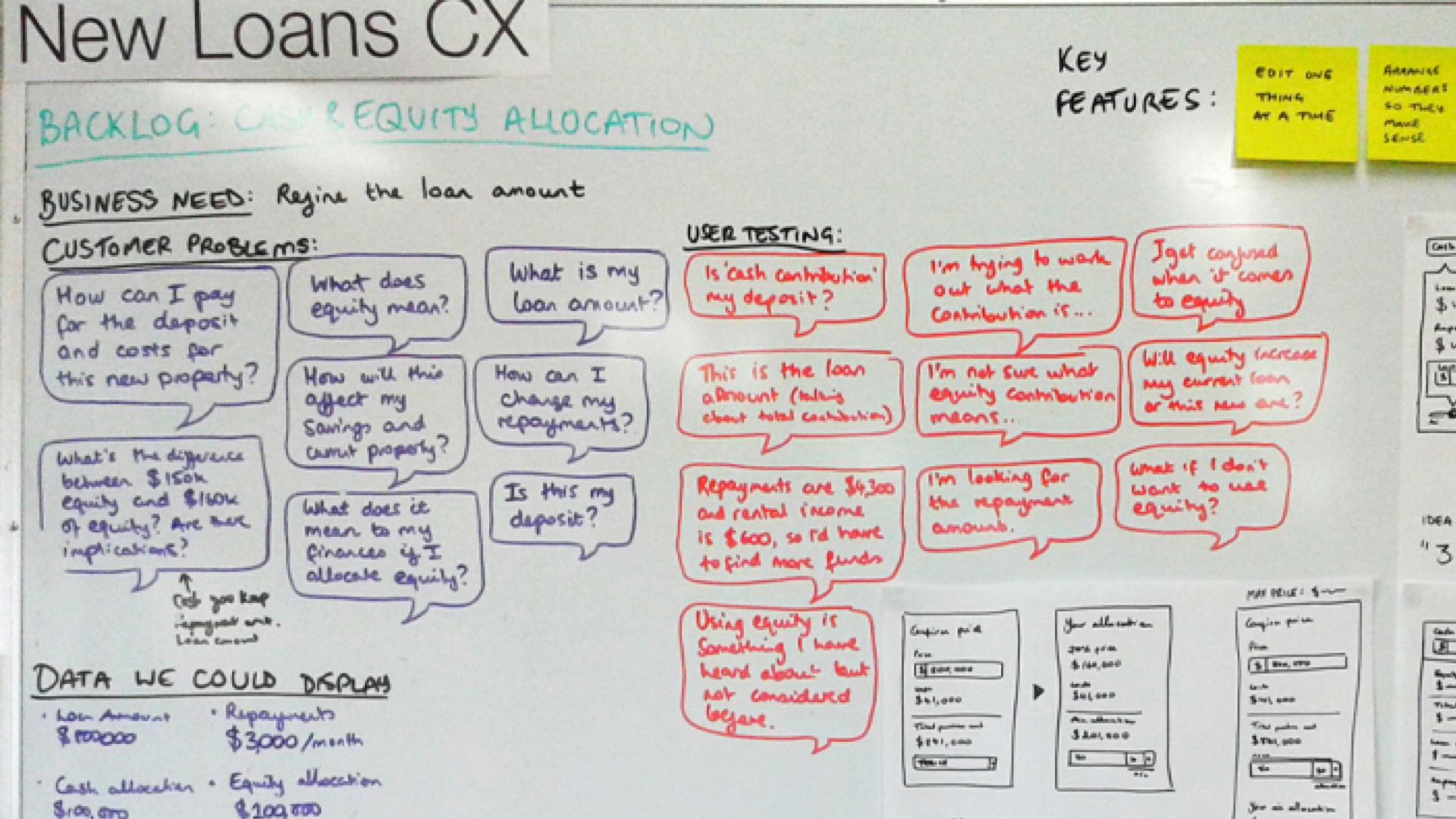

At the end of my involvement, design team had build out an extensive Discovery backlog with validated features that helped build out the product in the following months, some examples included:

- Build a relationship with a lender at their own pace through the interface.

- Verify options and borrowing amount (including tailored pricing).

- Access tools that help them narrow the property search and refine their scenarios.

- Options for their next steps, including existing equity and pre-approved borrowing amounts (including tailored pricing).

- Self manage loans online and access top up / variation immediately.

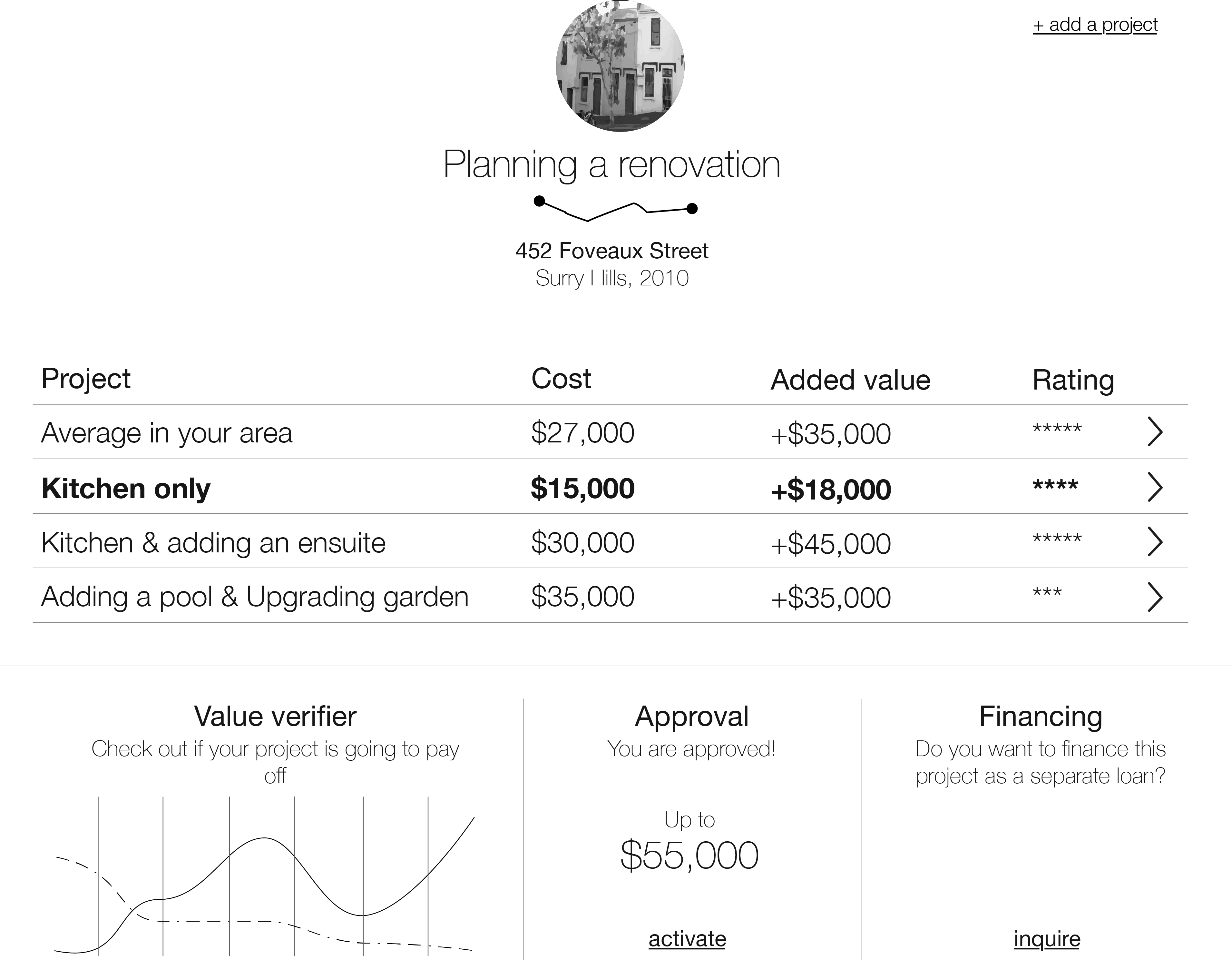

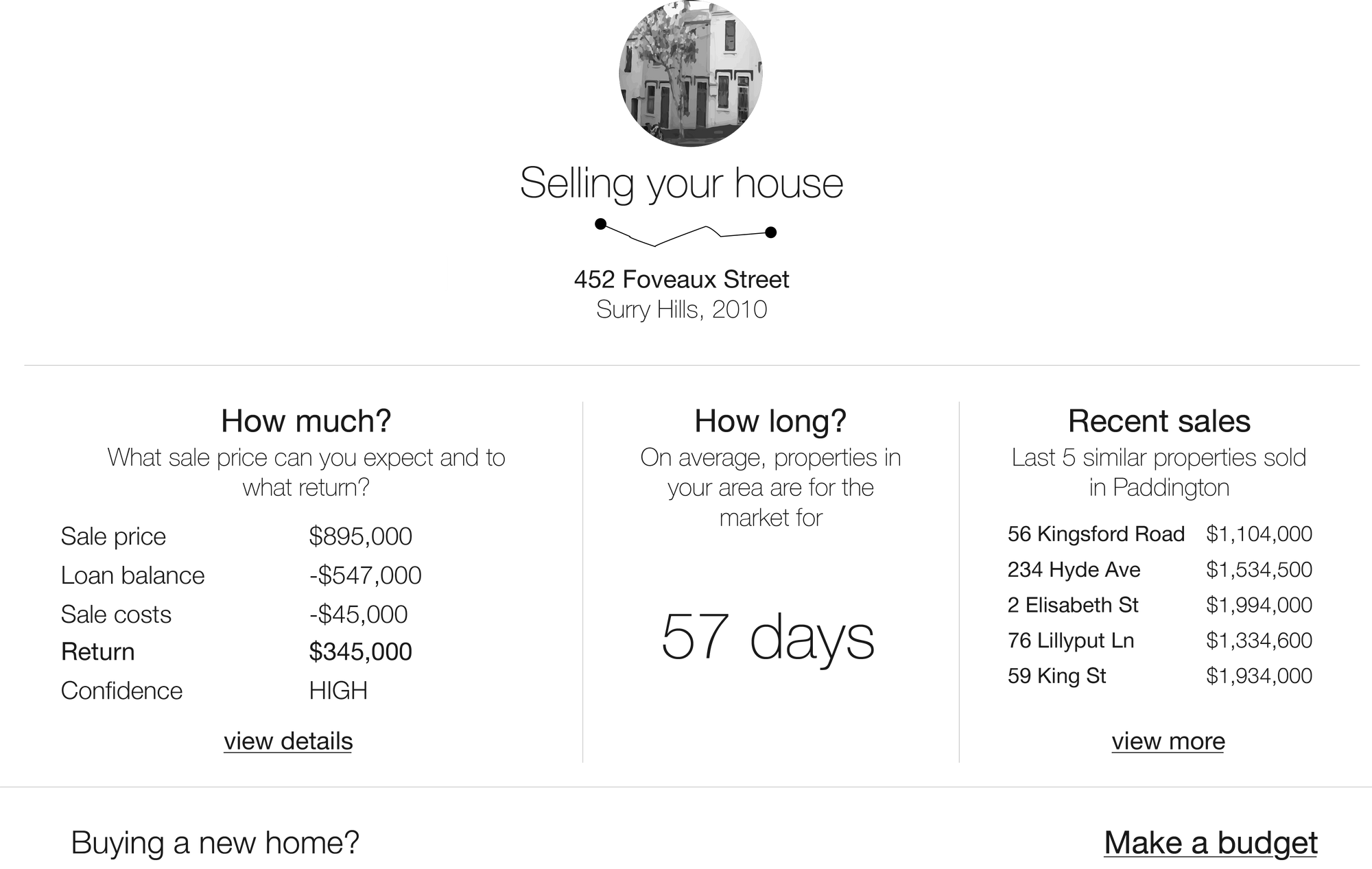

- Scenario planning (see wireframes below)

The concept testing mocks for "planning a renovation" and "selling your house" scenarios

Not only did Wonder assist customers, it also gives valuable time back to bankers in branch and call centres too. By reducing the need for capturing data, staff could instead focus on having meaningful conversations with customers.

Lenders now had shared access to the same information in a single system to assist delivering optimal service.

Outcome

Prior to Wonder, an approval in principal or indicative borrowing amount could take several days to process. Now, the process was instantaneous.

We won a Good Design Award in 2016 in the commercial services category!

With Wonder we have made things simpler, faster and easier for customers to understand exactly where they stand with their home loan and what they can do next.